I’ve had the same conversation dozens of times with business owners who are considering a sale.

It rarely starts with revenue multiples or deal structure. It starts with something harder to quantify: what happens to everything I’ve built?

Not the assets. The people. The culture. The reputation. The way the team shows up every morning and the way customers trust you to deliver.

For most business owners, the business isn’t a financial asset that happens to have some employees attached. It is an extension of who they are. The decision to bring on a partner or sell isn’t just a transaction. It’s one of the hardest decisions they will ever make — professionally and personally.

The fear is rational. The horror stories about private equity are real and well-documented. I’m not going to tell you they aren’t.

Research tracking post-sale outcomes finds that three-quarters of business owners who sell their company are dissatisfied with life twelve months later. Only about 7% of owners finish well — exiting on their own terms, with their legacy intact, feeling genuine satisfaction about what they built and how they passed it on.

Those are sobering numbers. But they aren’t inevitable. They are the outcome of choosing the wrong partner.

What You’re Actually Worried About — And Should Be

Every business owner I’ve spoken with has some version of the same concerns. The surface-level version is about price. The real version goes deeper.

Will the culture survive? The culture you built didn’t happen by accident. It took years of decisions — who you hired, who you promoted, how you handled hard situations, what you rewarded and what you refused to tolerate. You want to know it won’t be dismantled the moment the wire clears.

What happens to your people? The long-tenured employees who’ve been with you since the beginning. The ones who stayed through the hard years. You feel personally responsible for what happens to them. That’s not a soft concern — it’s the most important thing on your list.

Will you be pushed aside? Most PE firms will tell you during the courtship that they want you involved, that they value your expertise, that they aren’t going to upend the leadership team. Most of them mean it at the time. Then the reality of a diversified portfolio sets in, a new operator gets parachuted in, and the founder ends up with a title, no real authority, and a growing sense of regret.

These aren’t paranoid fears. They are the documented pattern of the industry.

Research from Revelio Labs, published by Bloomberg in 2025, found that nearly 20% of senior managers at PE-acquired companies are no longer with the firm within 18 months of close. A study tracking 2.5 million workers found that employees at PE-acquired companies earn an average of 18% less three years after the deal. Research from Oxford Said Business School found that Culture & Values ratings at PE-backed companies decline significantly post-acquisition — and the effect is worst for the longest-tenured employees, the people who remember how things used to be.

You have every reason to be cautious.

75%

Post-Sale Dissatisfaction

of business owners who sell their company are dissatisfied with life twelve months later

20%

Management Attrition

of senior managers at PE-acquired companies are gone within 18 months of close

18%

Average Pay Reduction

average reduction in employee earnings three years after a PE acquisition

The Price Is Not the Point

Your banker’s job is to run a process and get you the highest bid. That’s exactly the right job to do — if all buyers are equal. They aren’t.

Price is a threshold. Once you’ve determined that a price is fair and reflects what the business is actually worth, the questions that determine whether you made a good decision are not financial. They are questions about who owns the company next, what they actually know how to do, and whether their incentives are genuinely aligned with yours.

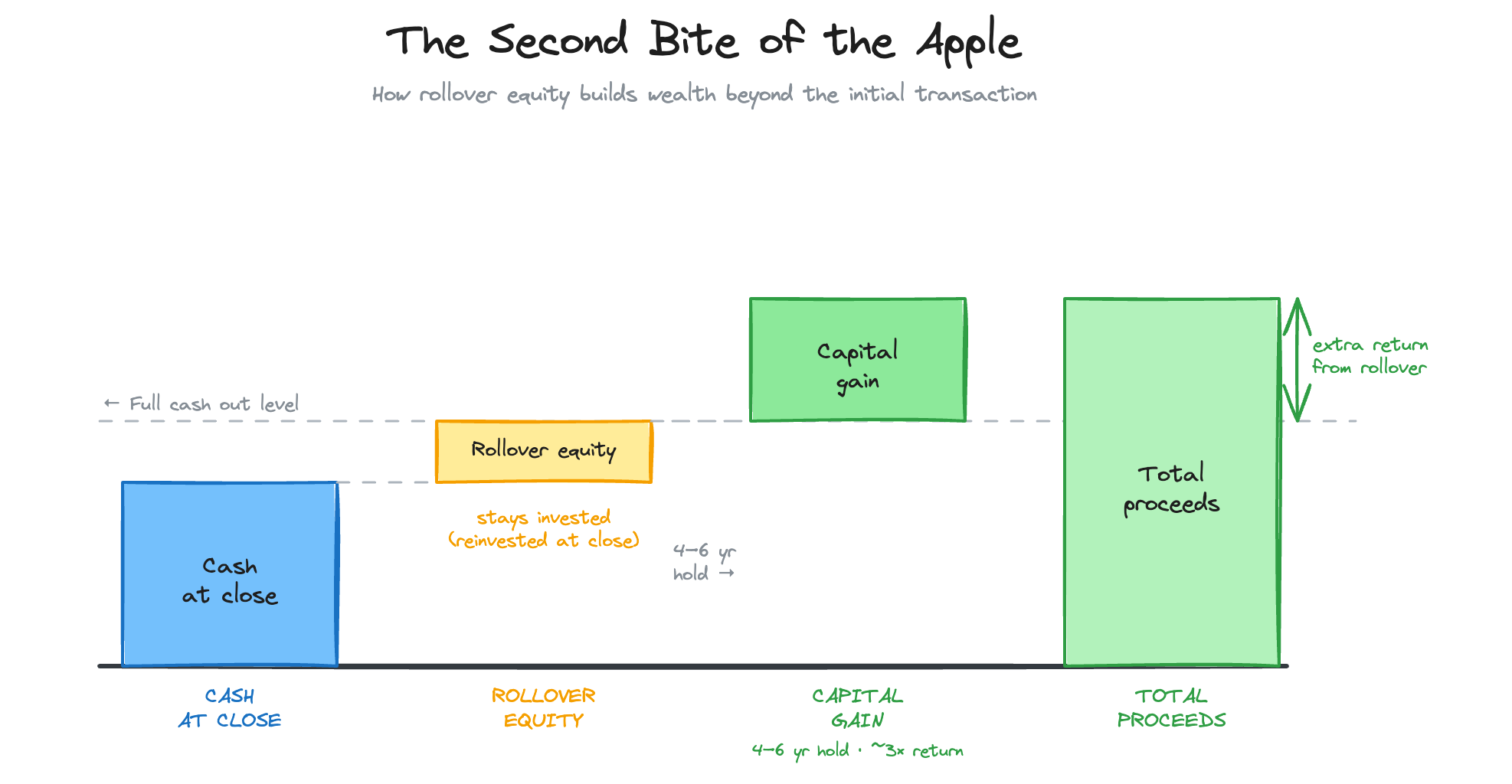

Here’s the structure I think about. At close, you have a fundamental choice: take all your chips off the table, or keep meaningful skin in the game through rollover equity.

Rollover equity means reinvesting a portion of your sale proceeds back into the company alongside your new partner, retaining an ownership stake rather than cashing out entirely. In the lower middle market, rollover equity typically ranges from 15% to 25% of total deal value — and its use has grown substantially, from 56% of North American buyouts in 2021 to nearly 68% in 2023, because it works for both sides.

Done right, the “second bite of the apple” — the return on your rollover equity when the company is sold again — is often equal to or greater than the initial close proceeds, on a fraction of the invested capital. More importantly, rollover equity changes the nature of the relationship. You’re no longer a former owner who sold. You’re an equity partner with aligned incentives, ongoing influence, and a defined financial stake in what comes next.

I structure every deal to maximize the seller’s rollover equity, not minimize it. A slightly lower upfront cash number with a larger ownership stake post-close is usually the right trade-off for owners who believe in what they’ve built and want to keep participating in the upside.

What a Real Partnership Looks Like

I should be direct about where Augeo Capital is different from most PE firms — and why those differences matter to the owners I work with.

Most private equity firms manage multiple portfolio companies across one or more funds. A partner at a mid-sized fund sits on four to six boards, with an associate staffed across multiple deals and a value creation team spread across the portfolio. You are one of twelve investments. In addition, they often have other funds they manage, and they are constantly fundraising for the next fund. The math on attention is not in your favor.

Augeo Capital builds a dedicated investment vehicle for each platform. Your company is not one of twelve. It is the investment. Every decision our capital partners make, every hour of operating attention we bring, every resource we commit — concentrated on one outcome: making your business significantly more valuable than it is today.

I also come to this work differently than most PE investors. Before Augeo Capital, I was a partner at McKinsey & Company, then a CEO running a middle-market portfolio company, then a PE operating partner. I have sat in the chair you’re in. I’ve made payroll when cash was tight, let go of people who didn’t deserve it, hired and fired executives, managed difficult customer relationships, and kept the business running through the 2008 financial crisis. When I work with you and your management team, I bring that experience directly — not a framework about it.

On leadership: I don’t parachute in a new CEO on day one. The people who built this business understand it better than any outside hire will for at least two years. My approach is augmentation, not replacement. We identify gaps — a CFO, a VP of Sales, an advisory board with relevant operating experience — and fill them in a way that strengthens the team rather than displacing it.

At some point, you will likely want to step back from the day-to-day. That’s normal. We’ll make that decision together, based on what is best for the company and for you. Once a new CEO is in place, you’ll continue to work with the board to help shape the strategy of the company, preserve its culture, and ensure that the company continues to grow and succeed.

What We Do for the Whole Team

The question I hear from almost every owner is some version of: what will happen to my people?

Here is my answer — not as a promise, but as a program we implement on every transaction.

We use the Three-Tier Ownership and Retention Architecture: a structured approach that extends economic participation in the business to every employee, from the front line to the leadership team.

T1

All Employees

Field staff · office · PM · corporate

Value Creation Units (VCUs) — phantom equity, 4–6% of post-acquisition equity, 4-yr vest / 1-yr cliff, fully accelerated at exit

At exit

T2

Leadership Team

Senior & mid-level leaders (top 25–30)

Profits interest or phantom equity, 7–9% of equity — 40% time-vested (4 yr), 60% performance-vested (unlocks at 2x / 2.5x / 3x MOIC)

At exit

T3

All Employees

Including acquired company teams

Pay increase · Enhanced 401(k) (immediate vest) · Certification bonuses · Safety incentives · Tenure milestones · Apprenticeships

Day 1

Tier 1: Value Creation Units for every employee

Every employee — field staff, office administrators, project managers, and corporate team — receives Value Creation Units (VCUs). These are phantom equity instruments that pay out in cash at a qualifying liquidity event, based on enterprise value growth above the acquisition baseline.

Four to six percent of post-acquisition equity is typically allocated to the VCU pool. Employees vest over four years with a one-year cliff, and the pool accelerates fully on exit. The cost to each employee is zero. The cost to the operating business during the hold period is zero — VCUs settle entirely from exit proceeds.

The goal is straightforward: every person who helped create the value being sold should participate in what the next chapter produces. Most companies we look at have no comparable program. The research validates why this matters: KKR’s ownership culture research found that employees who feel both engaged and like owners show 97% retention intent — compared to 47% for employees who feel engaged but don’t have ownership. That gap is not marginal.

Tier 2: Management equity with real performance linkage

Senior and mid-level leaders receive a separate equity pool — profits interest or phantom equity representing 7–9% of post-acquisition equity — with blended vesting. Forty percent vests on a time-based schedule over four years. Sixty percent vests based on exit performance: tranches unlock at 2x, 2.5x, and 3x MOIC (multiple of invested capital).

This is real equity, tied to outcomes that matter. The leadership team isn’t just retained — they are aligned with the same exit we are working toward.

Tier 3: Immediate impact on day one

Long-term equity is powerful. But employees feel it years from now. Tier 3 is what they feel on their next paycheck.

We implement cash programs at close: an across-the-board pay increase for front-line staff, an enhanced 401(k) match with immediate vesting and no waiting period, and certification bonuses with permanent hourly rate increases that stack and compound over time. We add safety incentive programs tied to team-level performance, tenure milestone bonuses that honor years of service without resetting the clock post-acquisition, and a formal registered apprenticeship program to build the next generation of skilled talent from within. Research on registered apprenticeship programs documents 90% retention rates and a $1.47 return on every dollar invested in training.

This is how we take care of people — not because it sounds good, but because it produces better outcomes for everyone, including our investors.

The Right Questions to Ask Every Buyer

If you’re running a process, or even having early conversations, here are the questions I’d encourage you to ask every potential buyer.

Ask them what they will do in the first 100 days. Generic answers — “we’ll professionalize operations,” “we’ll build infrastructure” — are a signal. Specific answers, with examples and named initiatives, indicate a real operating playbook. Vague commitments are easy to make. Specific ones require actual experience.

Ask them to name the three most common failure modes for businesses like yours. If they can’t answer this, they don’t understand your sector deeply enough. Pattern recognition from repeated experience is among the most valuable things an experienced operating partner brings. You want someone who has seen what goes wrong — not someone who has read about it.

Ask how they structure employee equity. If the answer is “we’ll evaluate that post-close,” it’s not a priority. If they have a designed program ready to implement at close, it is.

Ask how they’ve handled situations where the founder wanted to stay involved and the plan changed. Every honest answer to this question reveals something real about how they operate and what to expect.

The McKinsey “natural owner” framework — originally developed for corporate portfolio decisions — applies directly to sponsor selection: the best financial partner for your business is not the one with the most capital, the best brand name, or the highest bid. It is the one whose specific capabilities and experience make them uniquely positioned to maximize the value of your particular business. The highest bidder and the natural owner are often not the same party. The business performs better under the natural owner.

If This Resonates

Augeo Capital is not the right partner for every business or every owner. We work in a specific part of the market, with a specific type of company, and I’m straightforward about that.

But if what I’ve described here reflects what you’ve been looking for — a firm that is focused on your company, structured to align with your interests, and serious about the people who helped you build it — I’d like to have a conversation.

I respond to every serious inquiry. I’ll tell you within a week whether there’s a fit. No twelve-page NDAs, no six-month process to get a first meeting. Just a direct conversation between people who take this work seriously.

Start a conversation →