Many private equity firms will pursue any deal that clears their return hurdle. If the model works, they bid. If they win, they close. The implicit assumption is that capital is capital — that one dollar of equity is as good as any other, and that the sponsor behind it is largely interchangeable.

We disagree. And we think that assumption costs sellers, management teams, and investors a lot of money.

At Augeo Capital, we only pursue transactions where we believe we are the better owner of the business. Not a good owner. Not a capable owner. The better owner — the one uniquely positioned to maximize the long-term value of the company. When we cannot make that case to ourselves, we pass. When we can, we pursue the deal with conviction.

This is not a marketing talking point. It is a disciplined framework rooted in one of the most durable ideas in corporate strategy.

The idea behind it

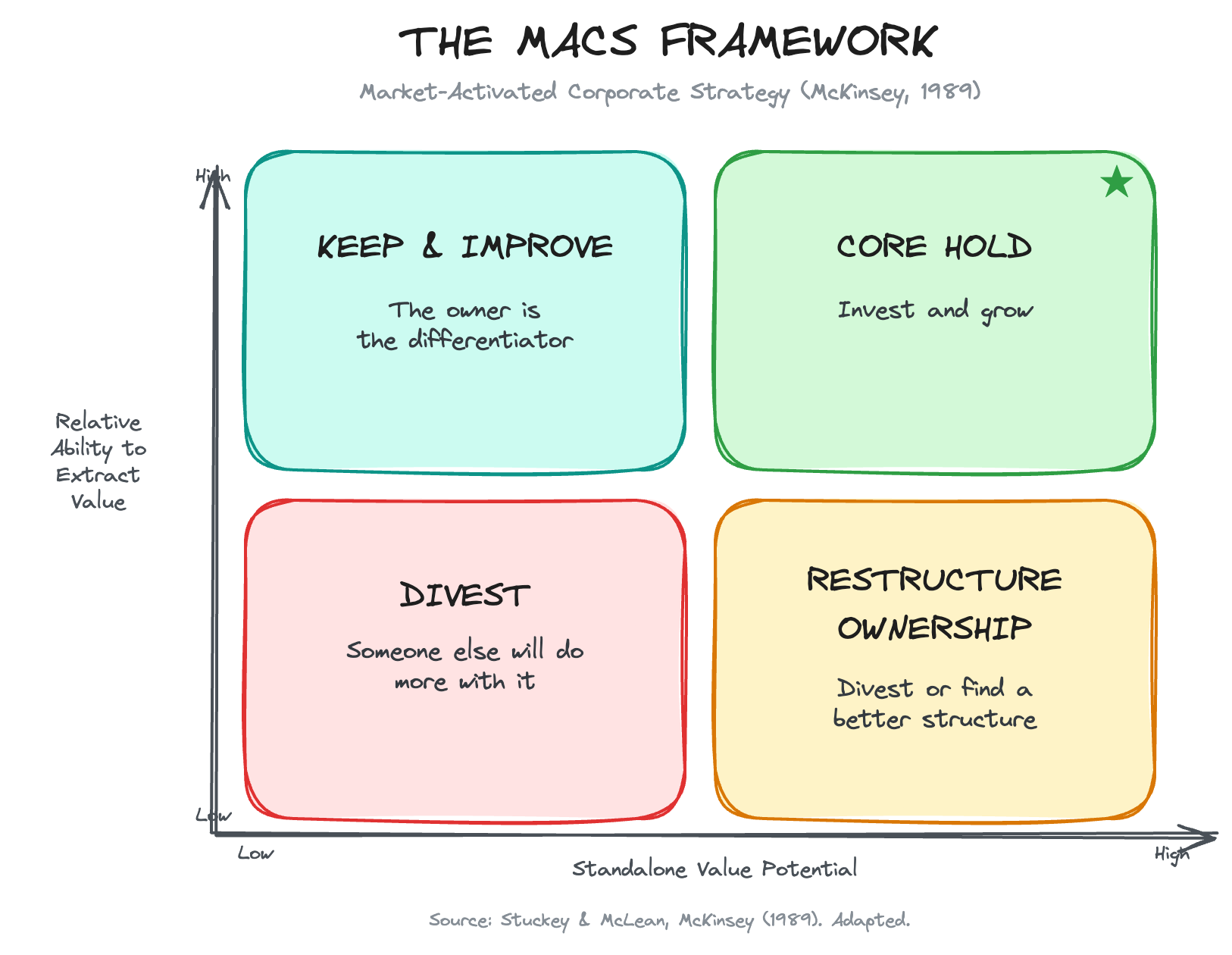

In 1989, McKinsey consultants John Stuckey and Rob McLean published an internal paper that introduced what became known as the “natural owner” principle. The core insight was deceptively simple:

Companies should own only those businesses for which they are uniquely positioned to maximize the net present value of future cash flows.

The paper was written during the twilight of the conglomerate era, when large corporations believed that diversification itself created value. Stuckey and McLean argued the opposite: what matters is not whether a business is attractive in the abstract, but whether you — specifically you, with your particular capabilities, resources, and expertise — are the best parent for it.

Owning a great business you cannot meaningfully improve is a worse investment than owning a good business where you are the better steward. The question is not “Is this a good business?” The question is “Are we the better owner for this business?” I might be biased, but I believe this is the only question that matters when making an ownership decision.

McKinsey later refined the language from “natural owner” to “better owner” — acknowledging that ownership advantage is not permanent. It shifts over time as industries evolve, capabilities change, and new owners emerge. The implication is that the question must be asked continuously, not just at the point of acquisition, and it also drives exit decisions.

The empirical evidence supports the discipline. McKinsey found that companies that regularly refreshed 10-30% of their portfolio through acquisitions and divestitures over a ten-year period outperformed the market by approximately 5%. Active ownership management — knowing when you are the right owner and when you are not — creates measurable value.

The natural owner principle was designed for corporate portfolio decisions, but it translates directly to private equity. The question every seller, advisor, and management team should be asking is: which financial sponsor will create the most value as the next owner of this business?

McKinsey identified four sources of ownership advantage. Each one has a direct parallel in how we evaluate whether we are the right sponsor for a given deal.

Operational synergies. Does the sponsor have the capability to work with the management team to identify and capture operational synergies? Can they help source and execute add-on acquisition and, more importantly, help to successfully execute post-merger integration activities?

Transferable skills and playbooks. Has the sponsor built a repeatable, proven approach — in sales, operations, technology, talent, or M&A — that applies to this business’s specific growth levers? The key word is specific. Every firm claims to “add operational value.” The question is whether the partners, as individuals, have done it before, at this scale, with proven results.

Superior access to resources. Does the sponsor have access to capital for follow-on investments and add-on acquisitions, a network of executive talent and functional specialists, and relationships with potential customers, suppliers, and partners that are difficult for the business to access on its own? In the lower middle market, where these resources are scarce, the sponsor’s network is often the single largest source of value creation.

Proprietary insights. Can the sponsor see things others miss — deep understanding of the business and operating models, pattern recognition from prior deals, or proprietary data that gives them an informational edge? The best owners know things about the industry that others do not — the three most common failure modes, the talent market dynamics, the regulatory risks on the horizon, the acquisition targets that are not yet on the market.

When we evaluate a potential investment, we are not just asking whether the business is attractive. We are asking whether we specifically — with our capabilities, our network, our playbook, and our experience — are better positioned than any other potential buyer to grow this business. If the honest answer is no, we pass.

At Augeo Capital, our strategic focus is clear. If a strategic buyer would be a better owner, we pass. If we lack the capabilities or industry understanding, we pass. If we cannot add value, we pass. We only pursue opportunities where our expertise aligns, and we can drive improvement.

Why this matters more in the lower middle market

In large-cap private equity, the difference between sponsors narrows. Businesses are more institutionalized, management teams are deeper, and capital itself is commoditized. The sponsor’s comparative advantage is often marginal — which is one reason large-cap deals are won primarily on price.

In the lower middle market, the opposite is true. The sponsor’s specific capabilities have outsized impact on outcomes because the businesses are at a stage where the right partner materially changes the trajectory.

Management teams are thinner. The CEO may also be the head of sales. The CFO may be a part-time controller. There is no HR function, no dedicated marketing team, no management bench. The sponsor’s ability to recruit, develop, and supplement talent is not a nice-to-have — it is a direct source of value creation.

Operations are less mature. There is often no ERP system, no CRM, no formalized sales process, no KPI dashboards. A sponsor with a specific, proven operational playbook can drive step-change improvements that would be incremental in a larger, more professionalized business.

Growth capital is harder to access. Lower middle market companies often cannot access institutional credit markets on favorable terms. An independent sponsor that creates a dedicated vehicle for the acquisition, with strong lender relationships, experience with lower middle market lending products, and the ability to raise incremental equity capital with no pre-defined cap, has a tangible advantage over one that does not.

Add-on acquisition is a primary value lever. Many lower middle market platforms are built through buy-and-build strategies. A sponsor with a track record of sourcing, closing, and leading post-merger integration processes is a better owner than one attempting it for the first time.

The relationship with the founder is decisive. In many lower middle market deals, the founder is rolling equity and staying involved post-close. Cultural fit, communication style, and alignment on the pace of change are not soft factors — they determine whether the partnership works or falls apart. A misalignment here destroys value regardless of the sponsor’s other capabilities.

These five dynamics create wide variance in outcomes depending on who the owner is. In the lower middle market, the sponsor is not a passive capital provider. The sponsor is an active ingredient in the business’s success or failure, and operators who invest present a unique value proposition to sellers.

What this means for founders who partner with us

This is where the framework matters most — to the people on the other side of the transaction.

In the lower middle market, most founders are not simply cashing out and walking away. They are rolling a meaningful portion of their equity into the new structure and continuing to lead the business alongside the new partner. The transaction is not an ending. It is a transition into a new chapter where the founder’s wealth creation is far from over.

When a founder rolls equity, they are making a bet — not just on the business they built, but on the sponsor they chose. The value of that rolled equity at exit depends entirely on how much the business grows under the new ownership structure. The founder’s second bite of the apple is only as valuable as the sponsor’s ability to grow the pie.

This is why the natural owner question is not abstract for sellers. It is the financial decision that determines their outcome.

A founder who selects the highest bidder but the wrong partner may get a larger check at closing — and a smaller outcome on their rolled equity. A founder who selects the right partner may accept a slightly lower upfront valuation — and end up with significantly more total wealth creation over the life of the investment.

The best outcome for a founder and their family is not the highest price. It is the highest total value created across both bites of the apple. And that total value is maximized when the sponsor is the better owner — the one whose specific capabilities, resources, and expertise will help drive the most growth and productivity improvements.

When we pursue a deal, that is the case we are making: not that we will pay the most, but that we will create the most. For the business, for its customers, for its employees, for the founder’s family, and for our investors. We take this responsibility very seriously.

The same principle tells us when to exit

The better owner principle is not just an investment filter. It is an exit discipline.

Every ownership advantage has a shelf life. The playbook that transforms a $100 million business into a $500 million platform is not the same playbook that takes it from $500 million to $2 billion. The talent network that fills a first VP of Sales role may not have the bench to recruit a full C-suite for a multi-division enterprise. The capital structure that funds three bolt-on acquisitions may not be the right structure for an international expansion or a public offering.

When we are honest with ourselves, the question is straightforward: are we still the better owner of this business, or has someone else — a strategic acquirer, a larger fund, a different type of sponsor — become better positioned to maximize its next phase of value creation?

The moment the answer shifts, holding on becomes value-destructive. Not because the business has deteriorated, but because another owner can now do more with it than we can. The discipline of letting go is as important as the discipline of saying yes.

For us, the exit signals are specific:

- The business has scaled beyond our operational sweet spot. We are built for the lower middle market. When a portfolio company grows into the upper middle market, it needs resources, governance, and capital structures that a larger sponsor is better equipped to provide.

- A strategic acquirer unlocks value we cannot. If a buyer can integrate the business into a larger platform — combining distribution networks, cross-selling into an existing customer base, or consolidating market share — they may be able to pay a premium that reflects real synergies.

- The next chapter requires capabilities we do not have. International expansion, complex regulatory environments, public market readiness — when the business’s growth path moves outside our core competencies, the right move is to hand it to an owner who has done it before.

This is the symmetry of the better owner principle. It tells us when to invest with conviction and when to exit with clarity. Both decisions serve the same purpose: ensuring the business is always in the hands of the owner best positioned to grow it.

We do not pursue every deal we can win. And we do not hold every investment until the last dollar of return has been squeezed out. We invest when we believe we are the better owner, and we exit when we believe someone else is. That discipline — applied honestly in both directions — is the foundation of everything we do at Augeo Capital.