Ask a room full of private equity professionals what drives top-quartile returns, and most will give you the same answer: sourcing. Find deals no one else sees. Pay less than market. The logic is intuitive — buy low, sell high — and the entire industry is organized around it. Firms build armies of business development professionals, invest millions in proprietary CRM systems, and measure success by the number of deals they see before anyone else does.

We are operators who invest. We think this conventional wisdom is incomplete. In some cases, it is flat wrong.

The proprietary-and-cheap playbook works for certain types of businesses — asset-heavy companies where the value sits in physical plants, equipment, or real estate. In those transactions, the seller walks away at close, the assets stay behind, and the purchase price is the primary determinant of returns. Buy it cheaper, and you make more money. Simple.

But that is not the kind of business we invest in.

When the people are the asset, the playbook changes

At Augeo Capital, we invest in business and industrial service companies. The key assets in these businesses are not factories or equipment. They are the people, the processes, the customer relationships, and the institutional knowledge that lives in the heads and habits of the team that built the company.

In a people-based business, the seller does not walk away at close. The founder typically rolls a meaningful portion of their equity and stays involved. The management team — often the same people who built the company from the ground up — continues to run the business day to day. Their engagement, motivation, and trust in the new ownership structure are not soft factors. They are the single largest determinant of whether the investment succeeds or fails.

This changes everything about how you should think about sourcing and pricing.

A founder who feels they were squeezed on price — who believes the buyer exploited an information asymmetry or a lack of competitive tension to get a deal — starts the partnership with resentment, not trust. They may have signed the papers, but they are not fully invested in the outcome. They will do what is required, not what is possible. And in a business where the people are the value, that gap between required and possible is where returns go to die.

In people-based businesses, the purchase price is not just a financial input. It is the first signal of how the partnership will work. A founder who feels they were treated fairly will run through walls for you. One who feels they were taken advantage of will do the minimum.

There is a corollary to the proprietary-deal orthodoxy: intermediaries are the enemy. They create competitive processes, drive up prices, and reduce the buyer’s edge. The ideal deal, according to this view, is one where no intermediary is involved and no other buyer knows the business is for sale.

We see it differently.

In today’s lower middle market, most attractive businesses come to market through intermediaries — investment bankers, M&A advisors, and business brokers. These professionals spend their careers helping founders work through the biggest financial decision they will ever make. Many have never sold a business before. They do not know what their company is worth, how a sale process works, or what to look for in a buyer. Intermediaries do the work that makes good transactions possible — educating sellers, preparing businesses for sale, and running processes that protect both sides.

As a focused, boutique firm, we will never have the reach and coverage of hundreds of high-quality intermediaries who spend every day talking to business owners in our target sectors and geographies. Trying to replicate that network through proprietary sourcing alone would be both inefficient and arrogant.

Instead, we have built deep, long-standing relationships with a selected group of intermediaries who understand our investment philosophy, our approach to value creation, and what we are looking for. They know the types of businesses where we believe we are the better owner. They know we will offer fair market value, move with urgency, and treat the founder with respect. And because they know all of this, they bring us the right deals — not every deal, but the ones where our specific capabilities give us a genuine edge.

Our intermediary partners are not a cost center or a necessary evil. They are an extension of our sourcing strategy. They see more businesses in a month than we could see in a year, and they know exactly which ones are right for us.

Fair market value is a strategy, not a concession

Here is where our approach diverges most sharply from convention.

Most private equity firms view the purchase price as the primary lever for generating returns. Pay less, make more. The entire sourcing apparatus — proprietary deal flow, off-market relationships, pre-emptive bids — is designed to create pricing advantages. The implicit message to the seller is: we are paying you less than you could get elsewhere, and we are doing it because we are smarter or faster or more connected.

We offer fair market value. Not because we have to. Because we choose to.

When you are the better owner of a business — when your specific capabilities, experience, and resources are uniquely positioned to help drive growth and productivity improvements — you do not need to buy cheap. Your returns come from what you do with the business after close, not from what you paid at close.

The purchase price is the cost of entry. The value creation plan is the source of returns.

This distinction is not semantic. It changes the dynamic with the seller from the very first conversation. When a founder knows that you are going to offer a fair price — that you are not trying to exploit a lack of competition or an information gap — they engage differently. They are more transparent during diligence. They share the real challenges and opportunities, not just the polished narrative. And they come into the partnership post-close already committed.

And that transparency, that commitment, that trust — in a people-based business, those are worth far more than a single turn of EBITDA you might have saved by negotiating harder.

Capital partners who understand the strategy

Our approach to sourcing and pricing only works if our capital partners are aligned. An investor who expects returns to come from buying cheap will be disappointed by our process — and they should invest with someone else.

The capital partners who invest alongside us understand something fundamental: our strategy to deliver superior investment returns does not depend on sourcing deals at below-market prices. It rests on identifying businesses where we are the better owner and executing a value creation plan that drives growth and productivity improvements — the only sustainable sources of value creation.

They understand that in the businesses we acquire, the founder and the management team are the most valuable assets. Being fair to those people — from the first offer through the life of the investment — is not a charitable act. It is a return-maximizing strategy.

Our capital partners dedicate time to understand the strategy and value creation plan we have developed for each business in partnership with its management team. They are long-term partners who are interested in creating lasting value through growth, productivity improvements, and investments in the company’s people and culture. They are not looking for a quick flip. They are looking for the same thing we are: businesses that will be meaningfully more valuable in five years because of the work we do together.

The sellers who choose us understand that we have sourced long-term capital from investors who, like us, are interested in building something real. That alignment — between sponsor, capital partner, and management team — is the foundation on which everything else is built.

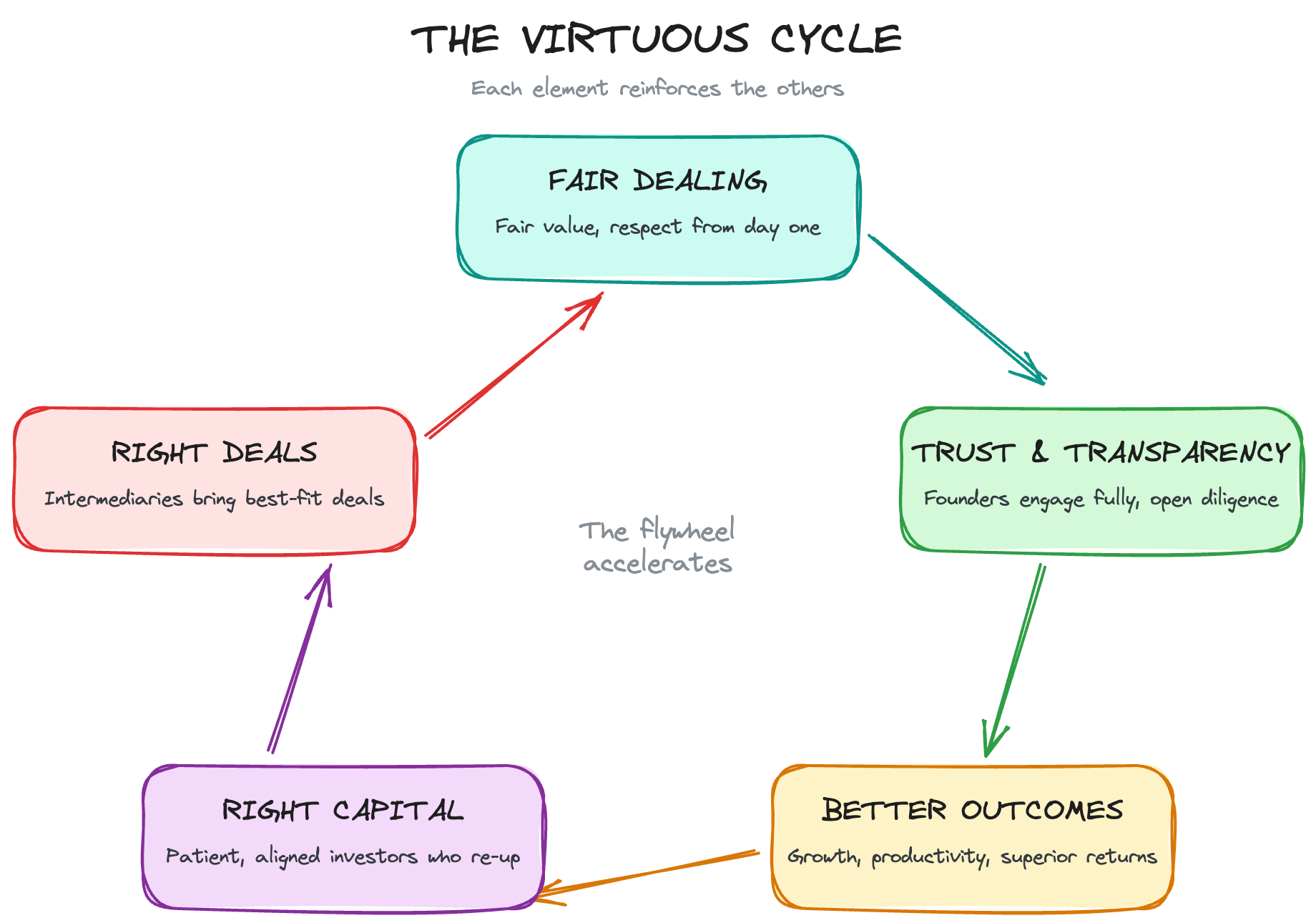

The virtuous cycle

When every element of the strategy is aligned, it compounds. Each piece reinforces the others.

Fair dealing with sellers builds trust. Founders who feel they were treated honestly become fully engaged partners, not reluctant participants. They bring their best ideas and their full energy to the post-close phase — which is where the real value creation happens.

That trust produces better partnerships. A management team that trusts its sponsor is more transparent about challenges, more open to change, and more committed to the plan. It translates directly into faster execution and better outcomes.

Better outcomes attract the right capital. Investors who see consistent, repeatable value creation — driven by operational improvement rather than financial engineering — re-up and refer their peers. They are also the investors who stay patient when the inevitable challenges arise.

The right capital enables the right strategy. When your investors understand and support the approach, you can afford to be disciplined. You can pass on deals where you are not the better owner. You can pay fair prices. You can take the time to do things right.

Intermediaries see the pattern. When advisors and bankers see that you treat founders well, pay fair prices, and create real value, they bring you more of the right deals. The reputation compounds. The deal flow gets better, not worse.

This is not a theoretical framework. It is a flywheel. And once it starts spinning, it accelerates.

There is no conflict

The conventional view presents sourcing and pricing as a zero-sum game: every dollar you pay the seller is a dollar less for your investors. If that were true, the only rational strategy would be to minimize what you pay — which is exactly what many in the industry try to do.

But it is only true if your returns depend on the purchase price. Ours do not.

Our returns depend on our ability to identify businesses where we are the better owner and to execute a value creation plan that drives growth and productivity improvements. That is where the alpha comes from. Not from paying 4.5x instead of 5.5x. Not from avoiding intermediaries. Not from exploiting information asymmetries. From the work we do after close.

The better owner principle is what resolves the apparent tension between being fair to sellers and delivering superior returns to investors. When you only pursue deals where you are the better owner, you can afford to pay fair value — because your edge is not in what you pay. It is in what you build.

We do not believe there is a conflict between treating sellers fairly and delivering top-quartile returns. We believe fairness is the strategy. When the people are the asset, trust is the highest-returning investment you can make — and it starts with the very first offer.